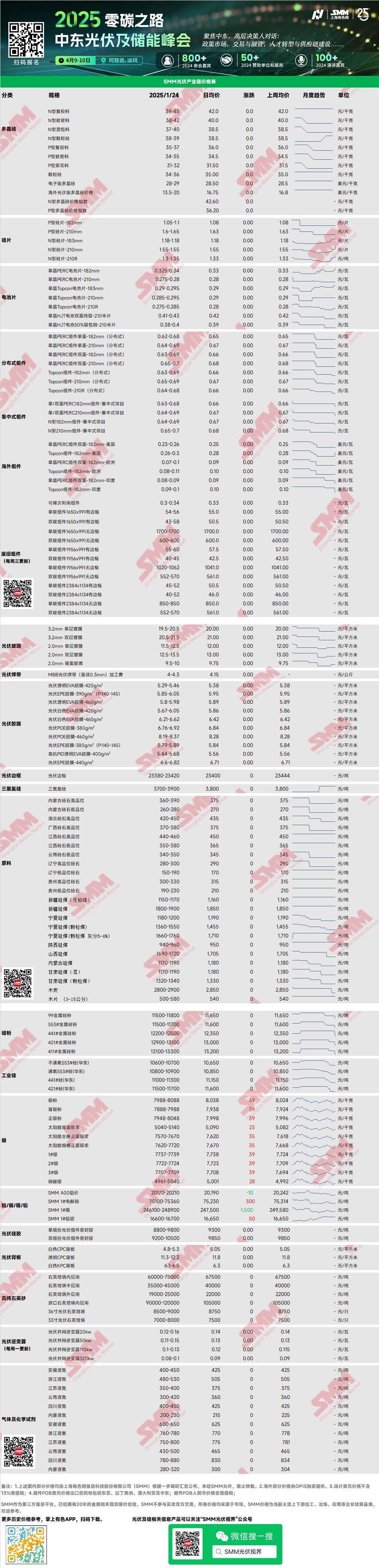

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon were 39-45 yuan/kg, and for N-type dense material were 38-42 yuan/kg. Polysilicon prices remained stable overall this week. Late last week, a leading enterprise completed a transaction of nearly 10,000 mt at approximately 41 yuan/kg, which is still within the mainstream transaction price range. The market sentiment was largely wait-and-see, with February production schedules varying among enterprises.

Silicon Wafers: This week, domestic N-type 18Xmm silicon wafers were priced at 1.18-1.18 yuan/piece, N-type 210R wafers at 1.3-1.35 yuan/piece, and N-type 210mm wafers at 1.55-1.55 yuan/piece. Silicon wafer prices remained stable overall this week. Resistance to high-priced resources persisted, and market transactions shrank significantly. The UFLPA list gained attention over the weekend and early this week, further fueling market caution. February production schedules are expected to increase slightly, driven by capacity expansion among integrated enterprises.

Solar Cells: Solar cell prices remained stable this week, mainly because module stockpiling and order signing were largely completed in mid-to-early January. New battery orders were limited, keeping prices steady with little likelihood of changes before the holiday. Some battery production bases began holiday shutdowns this week, but most battery manufacturers maintained operations, continuing production through the Chinese New Year. Prices for high-efficiency PERC182 solar cells (efficiency ≥23.2%) were 0.325-0.34 yuan/W; Topcon183 solar cells (efficiency ≥25%) were 0.285-0.295 yuan/W; Topcon210RN solar cells were 0.28-0.285 yuan/W; Topcon210 solar cells were 0.285-0.295 yuan/W; and HJT210 half-cell mainstream products were priced at 0.36-0.38 yuan/W.

PV Modules: In the current module market, mainstream transaction prices for centralized PERC182mm modules were 0.63-0.68 yuan/W, PERC210mm modules were 0.64-0.69 yuan/W, N-type 182mm modules were 0.64-0.69 yuan/W, and N-type 210mm modules were 0.65-0.7 yuan/W. The mainstream transaction price range remained stable. During the off-season, order volumes dropped significantly. Prices in the centralized market were relatively stable, while the distributed market saw prices stabilize due to reduced transaction volumes. Order deliveries were postponed to after the holiday or March. After the holiday, leading module enterprises plan to increase operating rates. Differences in orders on hand among enterprises for February were evident, with holiday durations ranging from 5 to 15 days. February operating rates are expected to vary, with overall production schedules projected to decrease slightly by about 1 GW MoM.

End-User: During the week of January 13-19, 2025, SMM statistics showed that domestic enterprises won bids for 28 PV module projects, with winning bid prices concentrated in the range of 0.65-0.71 yuan/W. The weighted average price for the week was 0.72 yuan/W, up 0.03 yuan/W from the previous week. The total procurement capacity awarded was 4,681.98 MW, down 2,208.41 MW from the previous week. Entering 2025, ground-mounted power station projects entered a lull, with progress slowing. Overall, Q1 remains a domestic off-season for demand, with limited installations expected before and after the Chinese New Year. Most orders scheduled for pre-holiday delivery are now postponed to after the holiday. Starting mid-February, orders are expected to increase slightly with procurement for centralized projects, with most demand accumulating in March. The implementation of new distributed policies is expected to drive a post-holiday rush for installations in residential and commercial-industrial projects.

Encapsulation Film: This week, prices for EVA transparent films were 12,600-13,000 yuan/mt, EPE co-extruded films were 15,000-15,300 yuan/mt, and POE films were 17,800-18,100 yuan/mt. Film prices remained stable. February prices will depend on post-holiday PV-grade EVA price trends.

EVA/POE: PV-grade EVA prices were transacted at 10,600-10,900 yuan/mt, while POE prices were 12,000-13,800 yuan/mt. Post-holiday bullish sentiment intensified stockpiling demand. The EVA spot market remains tight, and prices are expected to rise further. New domestic POE capacity is scheduled to come online in March, potentially leading to a downward trend in 4CPOE prices.

PV Glass: This week, PV glass quotations remained stable. As of now, mainstream quotations for 2.0mm single-layer coating glass are 12 yuan/m², and for 3.2mm single-layer coating glass are 19.5 yuan/m². In the final week before the holiday, PV glass trading volumes unexpectedly increased, with some leading module enterprises engaging in moderate stockpiling. According to incomplete statistics, January's glass trading volume exceeded module production by approximately 8 GW, leading to a slight reduction in glass inventory despite weak demand. However, during the Chinese New Year holiday, glass production will continue, while module production will decline due to holiday shutdowns. Glass inventory is expected to rise next week. In February, module pre-holiday stockpiling is expected to sustain high procurement volumes, leading to tight glass supply and a clear upward price trend.

High-Purity Quartz Sand: This week, domestic high-purity quartz sand prices remained stable. Current market quotations are as follows: inner-layer sand at 65,000-75,000 yuan/mt, middle-layer sand at 35,000-45,000 yuan/mt, and outer-layer sand at 19,000-25,000 yuan/mt. No significant transactions occurred in the domestic high-purity quartz sand market this week. On the supply side, leading enterprises reduced operating rates due to raw material constraints, while other sand companies also lowered production due to employee holidays and halted logistics. On the demand side, crucible enterprises reduced operations due to the holiday, weakening demand for quartz sand. Although silicon wafer production schedules increased slightly, crucible inventories remain sufficient, leading to low procurement willingness for quartz sand. Post-holiday negotiations are expected to dominate, with prices likely to remain stagnant.

Backsheet Weekly Review: This week, PV backsheet market prices remained stable at low levels. White CPC backsheets with dual fluorine coatings were priced at 4.8-5.3 yuan/m², while transparent CPC backsheets with dual fluorine coatings were priced at 11.3-12.3 yuan/m². As the Chinese New Year approaches, backsheet market activity remained subdued. Recent feedback from backsheet manufacturers indicated that conventional backsheet quotations were mostly above 5 yuan/m², with manufacturers showing strong price resistance.

According to market feedback, January's latest backsheet production figures were slightly below early-month expectations, with overall industry operating rates below 8%. Some leading enterprises indicated plans to reduce backsheet capacity this year, with annual production schedules expected to decline significantly compared to 2024. The backsheet industry continues to face weak supply and demand dynamics.

Inverters: This week, inverter price ranges were as follows: 20 kW models at 0.12-0.16 yuan/W, 50 kW models at 0.11-0.15 yuan/W, 110 kW models at 0.1-0.14 yuan/W, and 320 kW models at 0.09-0.11 yuan/W. Supply-side production remained stable and sufficient, while overall demand sentiment was mediocre. Post-holiday procurement and delivery demand are expected to increase significantly, with growing demand for residential models.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)